It’s kind of alarming how smoothly Apple made the transition to being a bank.

They’re slowly transitioning into the type of megacorp you usually only see in science fiction.

I don’t disagree, but it’s an important distinction to make that Apple is not the bank in this scenario. Goldman Sachs is the bank. Apple is basically just whitelabeling in the same way every store nowadays wants you to get their credit card. Macy’s giving you a credit card with their name on it does not make them a bank. Same goes for Apple.

and apparently GS wants out of the apple card business (according to some other report I saw)

so I wonder who would take over if they do leave

Chase and Amex are the biggest names in the game to step up currently. As long as it’s not Wells Fargo, it should be relatively the same for users, regardless.

They’re slowly transitioning into the type of megacorp you usually only see in science fiction.

Apple isn’t technically a bank in this case, but even if they were, it’s pretty common and not at all a dystopian sci-fi thing. Sony owns a bank. Hyundai owns a bank. In the US, GM made a bank over a century ago, spun it off in 2006 (it’s now called Ally), realized that was a mistake, and bought an existing bank in 2010.

Realistically once a business hits a certain size it’s practically a requirement. There’s not really a good way to be a company with a market cap of hundreds of billions, yet alone trillions and not at least act like a bank in a whole lot of situations. Might as well actually own one.

Apple’s fate is to be the American Sony

What does that even mean?

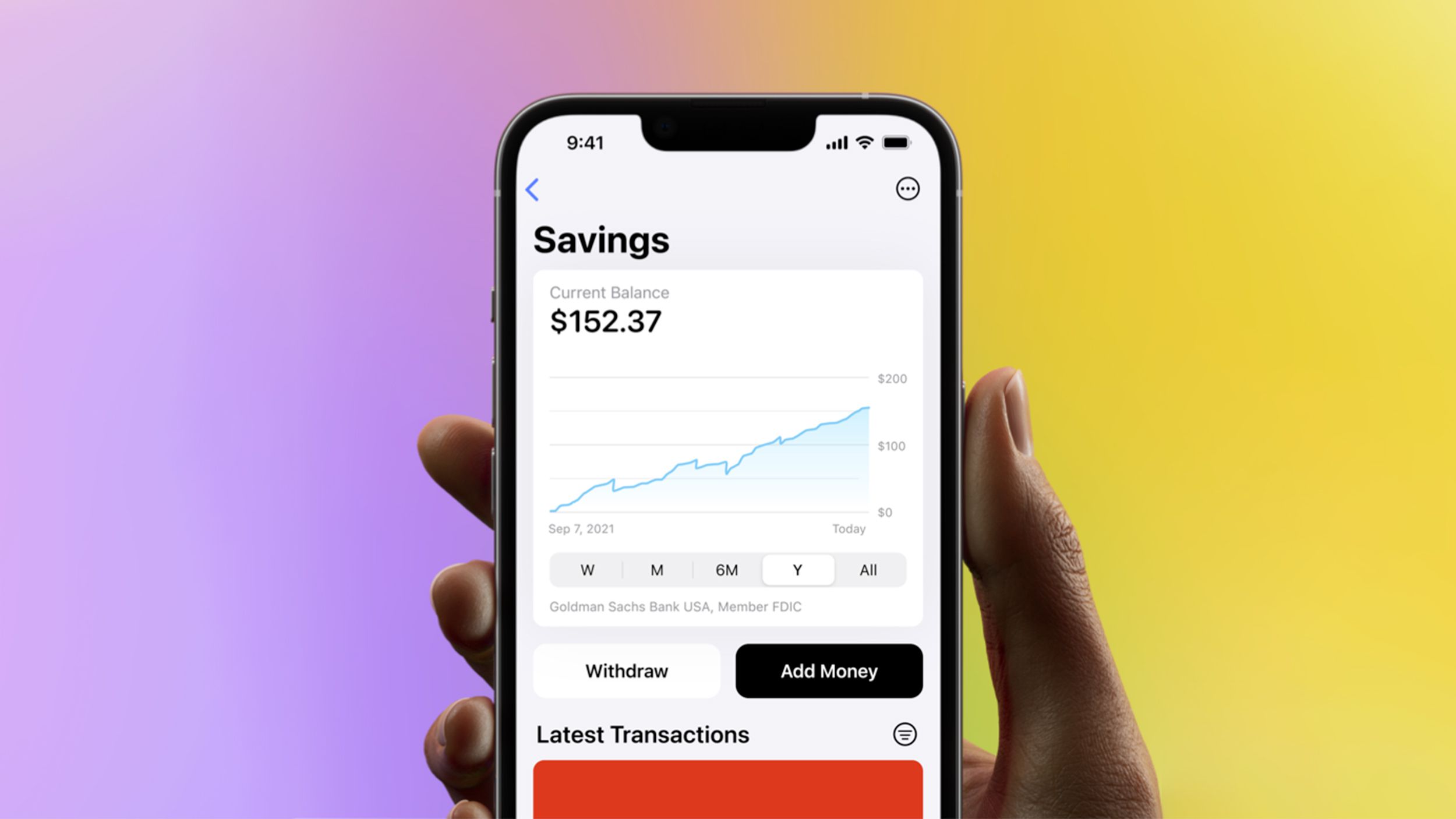

I kind of get it if the interest rate is 4.15% (assuming that that’s what APY means). Is this a common rate in the US? From my European perspective that’s incredibly high.

The Fed has massively increased interest rates in the past year or so to fend off a recession. That’s in part what led to the recent bank failures, because the banks made stupid investments hinging on low interest rates. As a whole, it’s been working wonders for the economy. Things have been stabilizing and fears of a recession have lowered.

In short, yes, 4.15% is on the good side, but it’s also pretty common in the US right now. Some savings accounts have 5%+ last time I checked, though those are harder to come by and often have stupid rules attached.

One minor correction, interest rates have been raised to fight inflation. Concerns of a recession came because when you raise rates people spend less and the economy slows. But, Americans being Americans, they haven’t really slowed down their spending so recession concerns haven’t been a huge issue.

My high street bank in the UK is also offering 4%.